In the dynamic economic environment of the UAE, business owners must understand tax regulations. It is not an alternative but a huge necessity. It’s more important than ever to stay updated with UAE tax regulations. This is especially in light of the most recent corporate tax implementation and the continuous complexity of VAT.

Any business, whether established or fresh to the region, may find it difficult to navigate the complex rules of UAE tax rates. As an integrated finance management platform, we help you understand the current UAE tax laws and how you can gain the right insights.

So, let’s get into the UAE tax laws that every business owner must know.

Corporate Tax Introduction

The UAE has announced its approval of a corporate tax rule that will get effect in June 2023. Businesses with profits over AED 375,000 are subject to 9% taxation.

Let’s discuss it more clearly,

- A 9% corporate tax rate has been imposed by the UAE on profits exceeding AED 375,000. This tariff is acceptable globally and aims to maintain the UAE as the leading economic center.

- There is a taxable income threshold of AED 375,000 in place. The exclusion of corporate taxes on profits below this threshold helps startups and SMEs.

Value Added Tax (VAT)

In January 2018, a flat rate of 5% was applied to Value Added Tax (VAT) in the UAE. It incorporates a wide range of products and services, with a few notable exclusions. It guarantees adherence to national tax laws and aids in prudent financial planning.

Also Read: What are the tax and VAT rules for influencers in Dubai? Here

Tax Implications for Specific Business Types

Depending on the kind of business you run, tax concerns in the UAE can differ significantly. What you should know is as follows:

1. Free Zone Companies

Companies are allowed to operate in “free zones,” which have been established by the UAE government and are subject to certain import, customs, and tax laws.

The tax exemptions available to businesses situated in these zones are among their primary benefits.

Companies founded in the United Arab Emirates’ free zones may be eligible for tax benefits, such as a temporary 0% corporate tax rate for a predetermined amount of time. This can be quite advantageous for startup companies and multinational firms trying to reduce their tax liabilities.

Businesses must understand that every free zone has a unique set of rules and incentives, though. The length of tax exemptions, the kinds of taxes excluded, and other perks about businesses can all differ.

Businesses that are already operating in or are thinking about establishing a free zone should carefully investigate and comprehend the unique regulations and advantages of the applicable free zone to maintain compliance and maximize their tax position.

2. Mainland Companies

Companies that conduct business on the mainland will have to pay the corporate tax that was established. On the mainland, businesses must budget for nine percent taxation on revenues above AED 375,000.

This tax rate makes prudent financial planning and management more important than ever for mainland businesses. Businesses must assess their present operational and financial frameworks to ascertain how this tax would affect their bottom line.

For tax optimization, it’s critical to consider a variety of tactics, including reassessing spending, assets, and income sources.

3. Offshore Businesses

In the UAE, offshore businesses are often excluded from corporate tax, income tax, and capital gains tax. However, they must abide by global tax laws and openness requirements.

The tax system in the United Arab Emirates treats offshore firms separately. These companies are favored by foreign investors and businesspeople due to their widespread exclusion from company tax, taxes on capital gains, and income tax.

The UAE uses this tax-friendly climate to draw in foreign capital and promote economic expansion.

It’s crucial to remember that even while offshore companies get tax breaks in the UAE, they still have some regulatory responsibilities. They must follow international tax rules and transparency requirements.

This involves abiding by tax information-sharing agreements, anti-money laundering laws, and other international compliance mandates. The goal is to ensure that these companies function within a legal structure that encourages openness and discourages tax avoidance.

Offshore enterprises need to comprehend and navigate these global regulations. Neglecting to comply may lead to legal ramifications and harm the organization’s image.

Consequently, offshore companies should consult professional legal and financial counsel. This is to ensure they fulfill all regulations and optimize the advantages of their tax-exempt status in the UAE,

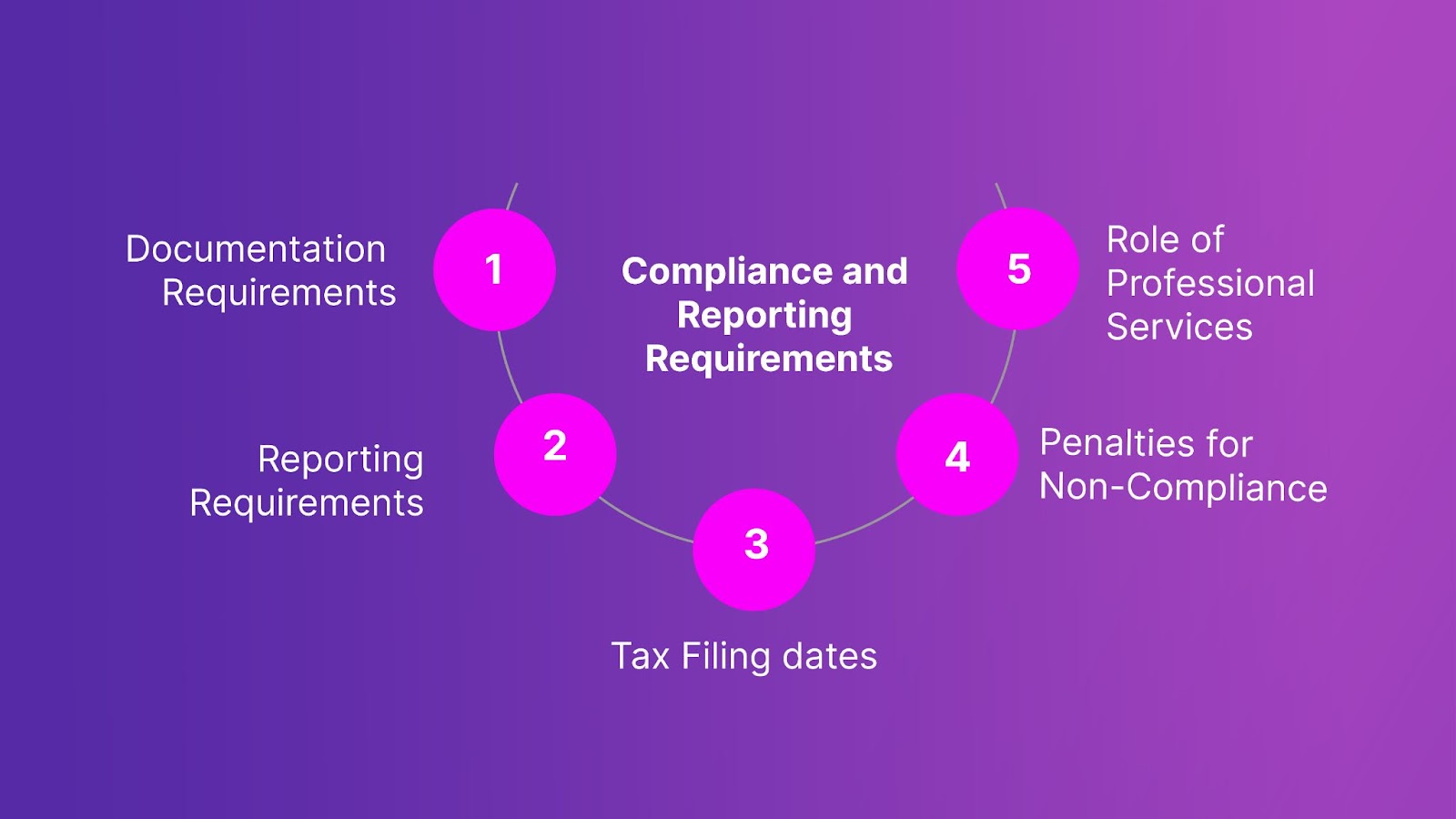

Compliance and Reporting Requirements

Businesses must navigate the UAE tax laws’ compliance and reporting obligations to avoid fines and guarantee efficient operations.

The essential information is outlined below:

1. Documents

Businesses must keep thorough and accurate records of all of their financial transaction management. This includes invoices, receipts, bank statements, and contracts. Both tax returns and audits need these documents.

2. Reporting

Every year, businesses are required to file tax returns with details about their income, expenses, and taxable profits. Various reporting formats and standards may be applicable, contingent on the type of the firm and the applicable tax legislation.

3. Tax Filing dates

To avoid paying fines for filing taxes after the deadline, it is essential to be aware of these dates. Depending on the type of tax and the fiscal year of the company, different deadlines may apply. Corporate tax returns, for example, are filed yearly, although VAT filings are usually done every three months.

4. Penalties for Non-Compliance

Heavy fines are imposed by the UAE government for breaking tax laws. Penalties, fines, and even a lawsuit could be part of this. The potential severity of the fines makes it imperative to make sure that all tax responsibilities are met.

5. Role of Professional Services

Managing tax compliance can be challenging, especially for companies with a wide range of operations. Professional services are essential for maintaining compliance. Businesses may manage their tax, accounting, and bookkeeping files more skillfully with our human + AI solution, which reduces the possibility of mistakes and non-compliance.

Tips for Tax Planning and Optimization

Firms need to prepare their taxes well to save taxes and boost earnings. To assist you take full advantage of your tax situation, consider the following techniques and advice:

1. Recognize Your Tax Responsibilities

Stay up to date with the latest tax laws and regulations in the UAE. This means knowing the corporation tax rate, the VAT legislation, and any applicable industry-specific tax advantages or reductions for your business.

2. Maintain Accurate Financial Records

Good tax planning requires precise, thorough bookkeeping practices. This entails tracking all earnings, outlays, and investments and organizing invoices and receipts for easy retrieval during tax filing.

3. Benefit from Tax Deductions and Credits

Find out which credits and tax deductions can help you reduce your taxable income. This could entail investing in research and development, cutting costs inside the organization, and receiving rewards for R&D work.

4. Consider Tax-Deferred Investments

Investing in tax-deferred accounts, such as investment funds or some retirement plans, can assist defer tax liabilities. This can ultimately reduce one’s overall tax burden.

5. Leverage Financial Management Software

Our integrated platform can help you find tax-saving opportunities, improve efficiency in your accounting procedures, and get real-time financial data. Additionally, it can guarantee financial reporting accuracy, which is essential for compliance.

6. Seek Professional Services

Professional services offering financial assistance can provide knowledgeable advice on tax optimization and planning. You can minimize your tax responsibilities while maintaining compliance as you negotiate the complexity of tax planning.

How Paci.ai Can Help Businesses in UAE Tax Laws?

The following are some ways that Paci.ai can help your company abide by UAE tax laws:

1. Simplified Tax Compliance

- Automated Tax Calculations: Paci.ai’s platform can calculate your taxes automatically, guaranteeing correctness and adherence to UAE tax regulations.

- Tax Registration Help: Companies who are not familiar with the tax system in the UAE can receive assistance from Paci.ai with the corporate tax registration process, ensuring that all necessary documentation is correctly filled out and organized.

- Preparing Your Tax Returns: The platform can help you prepare and file your tax returns, making the process easier and ensuring that it is filed on time to save penalties.

2. Professional Consulting Services

- Tax Consultation: Paci.ai’s team of tax specialists can help you manage the complexities of the tax system by offering individualized guidance on things to consider for UAE tax legislation, such as foreign income tax and the new corporate tax rate.

- Financial Advisory: Make the most of expert financial advice to improve your tax situation and make sure your business plans comply with UAE tax laws.

3. Customized Solutions for Expatriates

Paci.ai can offer customized tax planning solutions to minimize tax liabilities and guarantee compliance with UAE income tax regulations for foreigners for companies with foreign owners or employees, such as Indians in Dubai.

Final Thoughts

As we come to the end of our analysis of the complexities of UAE tax law, it is evident that, in a continually changing economy, a proactive and knowledgeable approach is essential. The implementation of company taxes and continuing modifications to the VAT laws have resulted in a transformation of the UAE’s tax regulations.

So, what wait? Paci.ai is the best platform for all your worries about UAE tax laws.

Connect with us right now to gain more updated knowledge on financial management.