A company’s success can be determined by how well its debt-equity ratio is balanced. We’re going to discover the idea of “Optimal Capital Structure” today. This is a crucial area of decision-making for companies of all kinds. However, what does it really mean, and why does it matter so much to your financial strategy?

Comprehending the complexity of ideal capital structure is essential for anyone involved in business. Let it be a CFO strategizing the next big move, a startup founder seeking to grow, or an investor assessing the health of the company. For sustained growth, strategic financial planning is more important than merely looking at the numbers.

Are you always tossing up whether to take out a loan or give up equity in your ownership? You are not by yourself. Our integrated finance service helps you in this. Every company, from small businesses to corporate finance, struggles to find the ideal balance between debt and equity. The aim? To increase firm value while maintaining costs at bay.

So, we can get into the blog and understand what is debt-equity ratio and the benefits of equity financing for startups.

Key Takeaways

- A lower WACC (weighted average cost of capital) is a way to reach the optimal capital structure.

- An optimal capital structure helps simultaneously maximize the market value of a company and minimize its cost of capital.

- There are differing views like that of experts such as Franco Modigliani and Merton Miller theorem that argue that the value of a firm is not impacted by its capital structure in an efficient perfect market.

Debt-Equity Ratio in the Current Market Scenario

A company’s total liabilities are divided by its shareholder equity to arrive at the debt-to-equity (D/E) ratio, which is used to assess the financial leverage of a business. One crucial indicator in corporate finance is the debt-to-equity ratio. It measures the extent to which a business is depending on debt rather than internal resources to fund its business activities.

Debt-equity ratio is calculated using the formula:

Debt-equity ratio = Total Liabilities \ Total Shareholder’s Equity

When a firm has a high debt-to-equity ratio, it is lending a greater amount from the market to support its activities. Conversely, when the ratio is low, the business is making use of its financial resources and lending fewer funds from the market.

Typically, the debt-to-equity ratio is higher in capital industries. On the other hand, sectors that are heavily reliant on technology and services may have lower DEs since they have fewer growth and capital requirements relative to other industries.

By definition, you can therefore conclude that a high debt-to-equity ratio is harmful to a business and is seen unfavorably by many analysts.

What Is Optimal Capital Structure?

A company is said to have reached the optimal capital structure level when its mix of debt and equity capital is in a certain proportion that minimizes the weighted average cost of capital. The average after-tax cost of capital from all sources of funds, including equity shares, preferred shares, and different forms of debt – of a company which in turn maximizes its market value. The lower cost of capital helps increase the present value of future cash flows.

Debt financing benefits from tax deductibility under tax regimes in most countries making the cost of debt capital lower than that of equity capital. This may not be currently applicable to the region, (it will be relevant when corporate taxation comes into effect from June 2023 onwards).

However, too much leverage (debt) exposes the company and its shareholders to higher financial risk and impacts the return on equity that shareholders expect. It also adds to interest payments, the volatility of earnings, and the risk of bankruptcy.

Thus, a company must formulate strategies toward reaching the optimal capital structure point at which the marginal benefit of debt equals its marginal cost.

The cost of debt capital is typically cheaper than equity because the former is relatively less riskier than equity. The reasons for this are that interest payments enjoy preference over dividends, and debt investors are settled before equity shareholders in the event of a liquidation.

In addition, the tax reliefs on interest make debt less expensive than equity. The dividend is paid out of post-tax profit in many countries. Another element in the optimal structure is using sufficient equity. This is to mitigate the risk of not being able to service and repay the debt considering the likelihood of volatility and uncertainty in the business and cash flow.

Building the Optimal Capital Structure

Most companies, particularly startups, prefer raising debt capital to equity to avoid equity dilution. The news about a company availing debt is typically considered a positive sign. In addition, too much addition of capital in a given time period will lead to a rise in the marginal cost of capital.

In addition to the weighted average cost of capital, there are a few other factors a company needs to consider while determining the optimal capital structure such as risk, expected return, industry or peer averages, debt/equity ratio, and credit exposure norms adopted by lenders, among others.

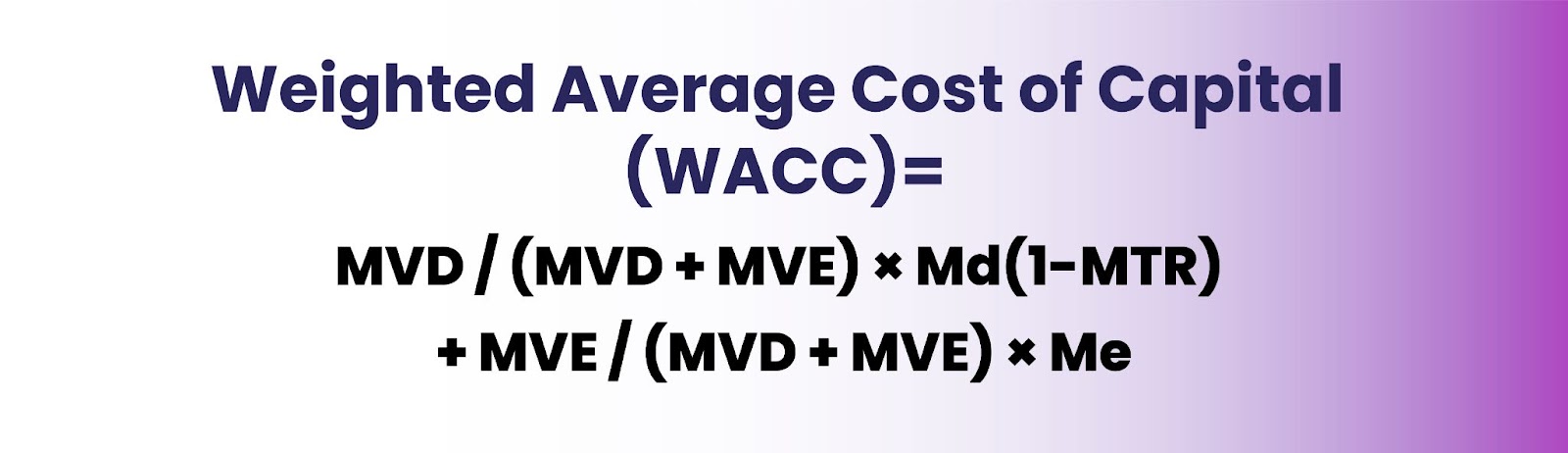

The WACC that could help build the optimal capital structure is calculated using the marginal cost of all the sources of capital employed and then computing the weighted average of all the costs of capital. The WACC for a company that has both debt and equity forming part of its capital structure is calculated using the following formula:

Weighted Average Cost of Capital (WACC) = MVD / (MVD + MVE) * Md(1-MTR) + MVE / (MVD + MVE) *Me

Where MVD = Market Value of Total Outstanding Debt

MVE = Market Value of Total Outstanding Equity

MVD + MVE = Total market value of the company’s combined debt and equity capital

MTR = Marginal tax rate of the company

Md = Pre-tax marginal cost of debt

Me = Marginal cost of equity

Because the interest is a tax-deductible expense in most countries, the WACC calculation considers the post-tax interest cost – Md (1-Mtr – of debt).

While debt capital has a lower cost than equity mainly because of the tax advantages, A high proportion of debt can lead to default risk making investors look for a higher return. This drives companies to structure the optimal blend of financing,

Hence, it refers to using the ideal proportion of equity capital to mitigate the risk of default that debt fund carries.

Theories on Capital Structure

Some views deviate from the conventional theories of the impact of optimal capital structure. Economists like Franco Modigliani and Merton Miller opined that in a perfect market, the capital structure will not have any impact on the value of the company and that leverage enhances the value of the company by reducing the WACC.

However, in the practical world, this is not the case. Because companies have to comply with tax rules, face credit risk, and incur transaction costs. This makes balancing the mix of debt and equity financing critical.

An alternative concept is the tradeoff theory. The theory assumes that companies can get benefits till companies achieve the optimum capital structure factoring in the tax advantage from interest payments, the cost of financial distress, and agency costs.

Another popular theory is the pecking order theory, which assumes that companies structure their financing strategy based on the path of least resistance. In this approach, it is assumed that internal financing is the priority, and debt and external equity financing are the last resort.

In nutshell

The optimal capital structure that companies seek must help them maximize the total value of the company while the cost of capital is minimized. However, in the real world, most companies want to balance the trade-offs between the benefits of debt and the risk of high leverage. This highlights the significance of the debt-equity ratio in the current market scenario.

A company must earn the minimum cost of capital to meet the minimum rate of return expected by the investors. This rate is used to discount the future cash flows expected to help estimate the present value (PV) of earnings on the investment of capital. Ultimately, a lower cost of capital means a higher present value (PV) of the business’s future free cash flows.

If you are looking for the best guidance on understanding financial management, you can contact us for further information.